UNDERSTANDING EQUITY FUNDS: YOUR ROADMAP FOR SMART INVESTING.

We have a lot of mutual fund categories be it equity, debt, hybrid, commodities, internation funds, Solution- Oriented, and many more other schemes which comes under Asset class, but understanding all together might create a confusion, instead we can focus on each type of fund, get familiar with all of the funds and there terms and later choose the funds which fits perfectly according to our needs and our investment portfolio.

So, first let’s have a look about what equity fund is, how it works, its types, benefits, etc……

Let’s get started, imagine your investment portfolio is a huge buffet, and you're building a plate for long-term growth. The main course? Equity funds, right? They’re the power players; they have been designed in such a way to turn your long-term goals into reality. But just like a main course has a variety of flavourful dishes, the world of equity funds offers a diverse menu, each with its own flavour of risk and reward. This blog will help you navigate this menu and choose the right "dishes" for your investment plate.

Equity funds are for investors with a long-term horizon and a higher risk appetite. They invest predominantly in company stocks, aiming to generate returns through capital appreciation. According to SEBI (Securities and Exchange Board of India) regulations, an equity fund must invest 65% or more of its total assets in equity and equity-related instruments. This standardization ensures that when you choose an equity fund, you know exactly what you're getting.

So, lets understand each of these funds:

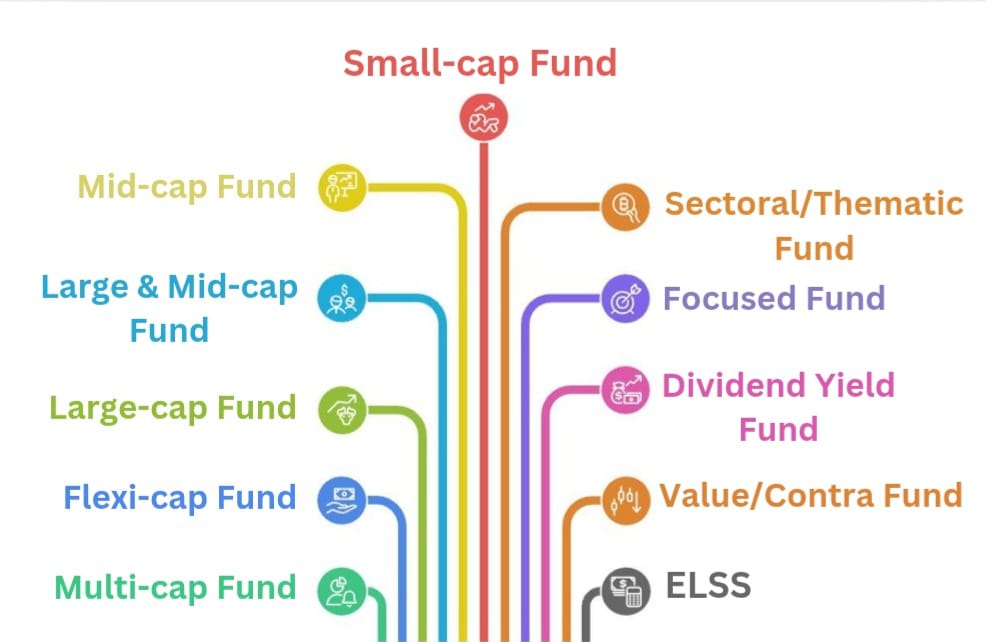

- The Building Blocks: Market Cap Categories

Understanding market capitalization is the first step. SEBI has officially defined three categories based on a company's size, creating a clear framework for investors.

- Large-cap Fund: These funds are often considered the "safe bet" of the equity world. These must invest at least 80% of their assets in the top 100 companies by market capitalization, such as Reliance Industries or HDFC Bank. They offer stability to your portfolio, as they're typically less volatile.

Example: The ICICI Prudential Blue-chip Fund, a large-cap fund, is one of the largest in this category based on AUM and delivered a return of over 22.1% in 2024 last 5 years CAGR return. This shows how large-cap funds can provide solid, stable returns while being less open to market swings.

- Mid-cap Fund: These funds must invest at least 65% of their assets in mid-sized companies (those ranked 101 to 250). These are fast-growing companies with the potential to one day become large-caps. They carry higher risk than large-caps but also offer the potential for higher returns.

Example: The Kotak Emerging Equity Fund has delivered a compounded annual growth rate (CAGR) of over 22% over the last 10 years, highlighting the significant long-term wealth creation potential of this category.

- Small-cap Fund: These funds invest at least 65% of their assets in small-cap companies (ranked 251 onwards). They are the riskiest of the lot and can be the top performer in one year and the bottom in the next. However, they hold the potential for exceptionally high returns over the long term.

Example: The Nippon India Small Cap Fund has delivered an impressive annualized return of over 34% (CAGR) over the past five years, showing how a high-risk approach can lead to explosive growth.

- Cross-Cap Funds: The All-Rounders

These categories were introduced to give fund managers more flexibility and to provide investors with a diversified, all-in-one equity solution.

- Multi-cap Fund: As per SEBI's mandate, these funds must invest at least 25% of their assets in each of the large, mid, and small-cap segments. This is a versatile choice that provides a balanced exposure and ensures the fund stays true to its label.

- Flexi-cap Fund: This is the more flexible option. Fund managers have the freedom to invest across market caps without any rigid allocation rules, as long as a minimum of 65% of the assets remain in equity. This immense flexibility allows the manager to dynamically shift the portfolio based on their view of the market, capitalizing on changing market cycles.

Example: The Parag Parikh Flexi Cap Fund is a leader in this category, with a large AUM, and its performance demonstrates the success of this dynamic strategy. It can move aggressively into small-caps during a rally or increase large-cap allocation during a downturn to provide stability.

- Large & Mid-cap Fund: This category offers a balanced approach, combining the stability of large-cap companies with the high-growth potential of mid-caps. According to SEBI rules, these funds must invest a minimum of 35% of their assets in each of the large-cap and mid-cap segments. This makes them a popular choice for investors who want a blend of stability and growth without the high volatility of a pure mid-cap or small-cap fund.

Example: The Motilal Oswal Large and Midcap Fund has a strong track record, with a three-year return of over 28%, showcasing how this strategy can deliver superior risk-adjusted returns by balancing both market segments.

- Strategic Funds: The Philosophers of Investing

These funds are for investors who prefer a strategy that goes beyond just market size.

- Focused Fund: For those who prefer a concentrated approach, these funds invest in a maximum of 30 stocks. They are designed for conviction-based investing, where the fund manager believes strongly in a select few companies.

While this can lead to superior returns, it also carries higher risk, as a poor performance in even one or two stocks can significantly impact the fund's overall returns. The history of this category suggests that it does not always provide a consistent return that justifies this higher risk.

- Dividend Yield Fund: This fund invests at least 65% of its total assets in stocks of companies that have a history of paying out good dividends. This fund is more for investors seeking a consistent income stream from their investments.

While it provides a steady income, this category has historically given a near-index return. For many, a low-cost index fund might be a more efficient choice for pure capital appreciation.

- Value Fund & Contra Fund: These funds invest a minimum of 65% in equity and follow specific investment philosophies. A Value Fund invests in stocks that are currently undervalued by the market but have strong long-term fundamentals. A Contra Fund takes a "contrarian" view, investing in stocks or sectors that are out of Favor with the market but are expected to perform well in the future.

SEBI's logic for having both categories is that a value strategy is, by its nature, a contrarian one. However, the history of this category does not show a consistent return that justifies the higher risk for a beginner.

- Sectoral / Thematic Fund: These funds must invest a minimum of 80% of their assets in a particular sector or theme. Sectoral funds invest in a specific sector (e.g., banking, IT), while thematic funds invest in a broader theme (e.g., infrastructure, consumption). They are highly concentrated and carry a lot of risk, as their performance is tied to the fate of a single sector or theme. A new investor should be cautious with these funds.

Example: The Tata Digital India Fund is a thematic fund that has delivered an impressive annualized return of over 20% over the past five years, capitalizing on the growth of India's digital economy.

- Specialized & Tax-Saving Options:

- ELSS (Equity Linked Savings Scheme): The tax-saving option. These funds come with a 3-year lock-in period and are the only equity funds that offer tax deductions under Section 80C of the Income Tax Act. It's a powerful combination of tax-saving and wealth creation. The mandatory lock-in period for ELSS prevents impulsive redemptions and encourages disciplined, long-term investing.

Investments in an ELSS fund are tax deductible under Section 80C of the Income Tax Act of 1961. While there is no upper limit on the amount that can be invested, the IT Act allows for a tax deduction of up to Rs. 1.5 lakh. Investing this amount in an ELSS can result in tax savings of up to 46,800 per year.

Example: The Mirae Asset ELSS Tax Saver Fund has delivered a 5-year return of over 24%, proving that you can achieve both significant tax benefits and wealth creation.

Building Your Equity Plate

The mutual fund choice set is vast, but it's not meant to confuse you. It’s designed to give you the tools to build a portfolio that is uniquely yours. By after understanding these different categories and their characteristics, you can make decisions that will help you build your portfolio. Don't just blindly pick a fund; create a strategic mix of equity that aligns with your financial goals, your timeline, and your comfort level of risk. Happy investing!

Note (Please Read)

Mutual funds are subject to market risk. Read scheme documents (SID/KIM/factsheet) carefully. Past performance does not guarantee future results. Choose funds that match your goals, time frame, and risk tolerance.

.png)

.png)

.png)

.png)

.png)